BondWorld : Bulls at the test of central banks. European peripheral bonds more vulnerable

Abonnieren Sie unseren kostenloser Newsletter

Andrea De Gaetano – Independent Analyst

BondWorld – All rights reserved

Crucial week, with monetary policy decisions by the FED, ECB, BOE, BOJ and 19 other central banks.

Omicron variant and prospects of monetary tightening are worrying.

On the other hand, corporate earnings, buybacks and near-zero interest rates are supporting equity prices.

A reduction in central bank purchases could revive volatility. Volatility has fallen in equities but remains high in US Treasury options. Investors are buying insurance to protect themselves against an adverse movement in US government bonds, with the Merrill Lynch Option Volatility Estimate (MOVE) at 78, close to its highest level for a year.

U.S. inflation at 6.8% in November, the highest level since 1982, and unemployment at 4.2% reinforced expectations of tapering by the Fed.

On Tuesday 30 November, Jerome Powell said in a hearing before the US Senate that he no longer sees inflation as ‚transitory‘. Higher than expected inflation in November confirms Powell’s words.

However, the market did not seem spooked by Powell’s words.

Treasury bonds shrugged off the release of inflation data at 39-year highs, with yields falling on the long end of the curve. Thirty-year yields fell from 2.50% in March to 1.85% today.

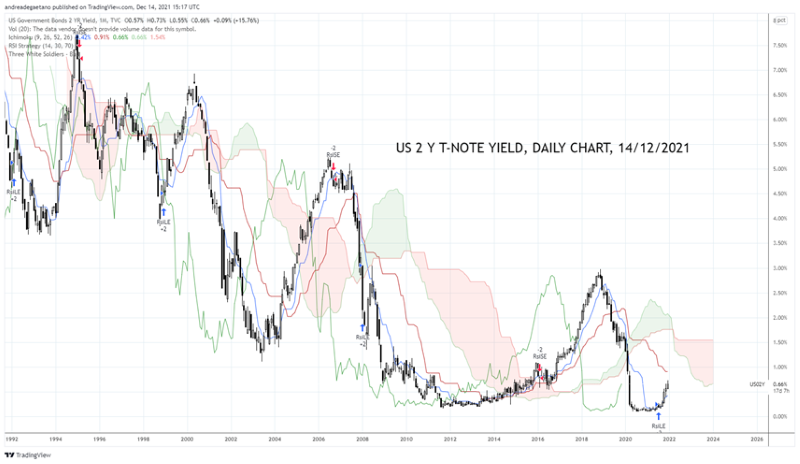

Yields up on short maturities: the 2-year rose from 0.11% in March to 0.66% today. Sixfold increase in less than 9 months.

Historically, the flattening of the yield curve anticipates periods of economic slowdown.

Christine Lagarde, who has remained dovish, now finds herself under pressure, with Covid and inflation on the rise.

„The negative effects of bond purchases are increasing, while the benefits are fading,“ argues Isabel Schnagel, ECB executive member in charge of market operations. While in favour of a reduction in purchases, Schnabel highlights the risk of „fragmentation of the euro area“.

Words that evoke a widening of credit spreads, of which there are already hints.

The market’s expectation is that the „flexibility“ announced by Christine Lagarde will translate into a switch from the emergency PEPP programme, which will end in March 2022, to the pre-existing PAP purchase programme.

Seeing what has happened in countries that have raised or lowered rates too much, one understands the caution of the Fed and ECB.

Brazil has entered a technical recession. To quell inflation, at 11%, Brazil’s central bank raised rates by 1.50%, the biggest interest rate hike in 20 years, to 7.75% (in March 2020 they were at 2%). This coincided with an economic contraction of 0.1% in the third quarter compared to the previous quarter, which had already contracted by 0.4%.

At the other end of the spectrum, Turkey’s central bank. Driven by Erdogan, despite inflation above 21%, it cut rates from 19% to 15% and drove the Turkish lira into collapse.

The Euro/US Dollar exchange rate, compressed between 1.12 and 1.14 for about a month, is waiting for the central banks‘ traffic lights to take a direction, which will take shape below 1.11 or above 1.1450.

The view of more aggressive Fed than ECB plays in favour of dollar, but it might be already discounted in prices, which is why we have been easing dollar in recent weeks.

The Fed and ECB will be cautious and barring some short-term jolts, markets still look well in tune. The euphoria has passed, but it is too early to talk about a recession. For now, despite the slowdown, the economy and corporate profits are expanding and central banks are accompanying the market.

Lighter, but we remain invested.

Quelle: BondWorld.ch

Newsletter